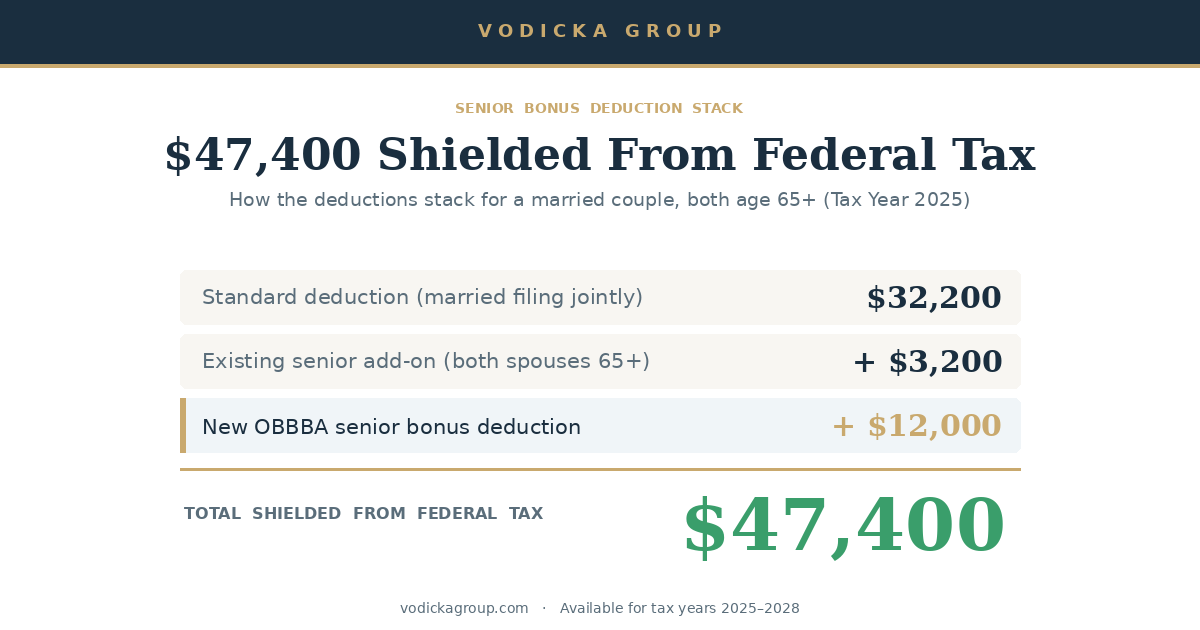

*Energy stocks have been weak for the last year. But with earnings holding up and crude on the rise, the long-term valuation looks compelling.

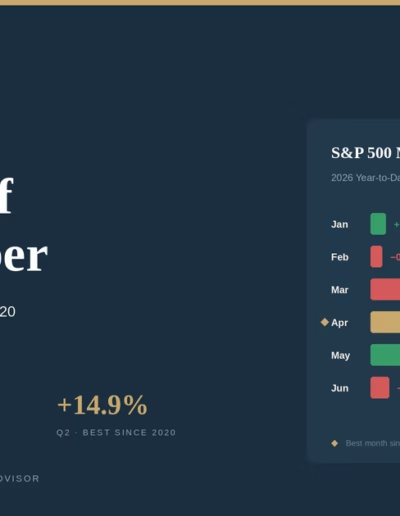

The market has had a great year, with the S&P 500 (SPY) posting its best first quarter in 14 years. That rising tide has lifted all boats, particularly energy, helping the sector to recover from a tough second half of 2011.

But in spite of the rebound, energy stocks still look undervalued on a historical basis. That’s because last year’s sell off was much sharper than any deterioration in earnings or long-term fundamentals. And with crude prices on the rise and a weak dollar, there are more than a few reason to be taking a close look at energy stocks as the group remains mostly out of favor with the Street.

So on that note, here are Top 5 energy stocks with the right mix of growth and value.

Top 5 Energy Stocks

Carbo Ceramics (CRR) is down more than 44% from its all-time high above $180 in August. With a forward P/E of 16 against the 10-year median of 23X and analysts looking for 34% earnings growth next year, this is the sweet spot of growth and value.

Carbo 1-Yr Chart

Stone Energy (SGY) is green on the year, but shares still only trade at 7X forward earnings, a huge discount from its peers and historical levels. As an exploration and production company, SGY stands to benefit from higher crude and natural gas prices.

Petterson UTI, Inc. (PTEN) has been an energy laggard in 2012, falling into the red as estimates fall. But in spite of that weakness, with a forward P/E of 7.2X, PTEN also trades at a discount to its peers and historical levels.

Haliburton (HAL) is another energy stock trading in the red for the year, as lower natural gas prices have hurt drillers and service providers. But HAL’s forward P/E of 9X is less than half of the 10-year median of 19X. Analysts are looking for 16% earnings growth next year.

Exxon Mobil Corp (XOM) is our pick from big oil, currently trading with a forward P/E of 10.5, safely below the 1-year median of 12.3. And with a nice 2.2% dividend, shareholders get paid to own this stock.

The Take Away

There’s no doubt the energy trade is still out of favor with the market. It’s been like that for a while, since last spring. But with the earnings and fundamental picture still intact, it could be a good time to buy energy stocks while the rest of the market yawns.

Michael Vodicka is the president and founder of the Vodicka Group, Inc., a Registered Investment Advisor (RIA). He specialized in trading fixed-income derivatives at the Chicago Board of Trade before spending five years managing equity portfolios for a private investment research company.

Michael graduated from the University of Kansas with a degree in business communications and is registered with the State of Illinois and the SEC (Securities and Exchange Commission) as a Licensed Investment Advisor (Series 65).