READING TIME: 8 MINUTES

The S&P 500 weathered a bout of Q1 2026 volatility driven by geopolitics — not fundamentals. The bull market is intact, earnings are accelerating, and here are four strong reasons the stock market outlook for the rest of 2026 looks bright.

S&P 500 Q1 2026: What Happened

The S&P 500 (SPY) had a turbulent first quarter — but let me be clear upfront: the big picture remains very encouraging. After hitting a fresh all-time high of 7,008 on January 28th, the index pulled back roughly 9% peak-to-trough before stabilizing. It closed Q1 down about 4.4% for the year. As of today, we’ve already bounced back to around 6,609.

That kind of drawdown is completely normal. Since 1980, the average intra-year pullback for the S&P 500 is about 14% — and the market still finishes higher in roughly three out of every four years. A single-digit dip after two consecutive years of double-digit gains is the market catching its breath. It is not a reason for concern.

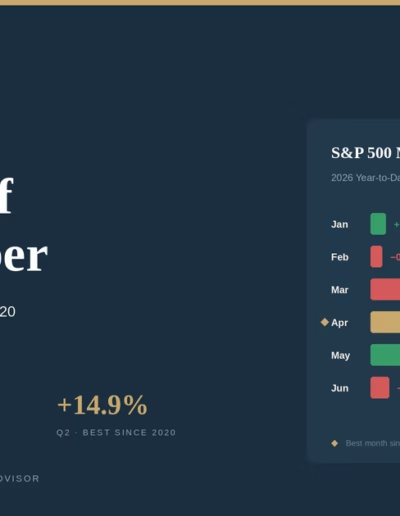

Monthly S&P 500 Returns — Q1 2026

January held gains before geopolitical headwinds pulled markets lower in February and March.

Jan

+1.4%

Feb

-0.8%

Mar

-5.0%

More importantly, the fundamentals that power this bull market have not changed. Corporate earnings are growing at a double-digit pace. The U.S. economy continues to expand. AI investment is accelerating at a historic rate. The bull market that began in October 2022 is now up approximately 92% — and while there will always be bumps along the way, the underlying foundation remains as strong as it’s been in years.

What Drove the S&P 500 Q1 2026 Pullback?

There were three main factors behind the selling pressure in Q1. Let’s walk through each of them — and why none of them change the long-term stock market outlook for 2026.

1. The U.S.–Iran Conflict Rattled Markets

This was the biggest driver of the Q1 pullback. In late February, the United States and Israel launched large-scale airstrikes on Iran targeting military and nuclear facilities. The conflict escalated into a broader Middle East confrontation, sending oil prices sharply higher and reigniting inflation fears. Treasury yields jumped, risk appetite dropped, and March saw a swift 5% decline as investors moved into de-risking mode. The good news: geopolitical disruptions like this have historically been temporary — and markets tend to recover quickly once the dust settles. We are already seeing stabilization in early April.

2. Tariffs Created Headline Noise

Trade policy uncertainty continued to weigh on sentiment in Q1. Markets don’t love policy unpredictability, and that showed up in investor caution. However, tariff headlines tend to be louder than their actual economic impact — businesses adapt, trade flows adjust, and negotiated outcomes typically follow the initial announcements. This is something to monitor, not something to lose sleep over.

3. Tech Took a Breather

Technology led the market higher in 2024 and 2025, and it was the biggest drag in Q1 2026. The NASDAQ underperformed the broader index as investors rotated out of high-multiple tech names after a massive multi-year run. Some of this is normal profit-taking — and some of it is the market asking whether AI stock growth can justify stretched valuations. Importantly, the answer from the earnings data so far is: yes, it can.

“The bull market is up 92% since October 2022. A single-quarter pullback of 4.4% is not a crisis — it’s the market catching its breath before the next leg higher.”

— Michael Vodicka, The Vodicka Group

S&P 500 Earnings Growth: The Engine Keeps Running

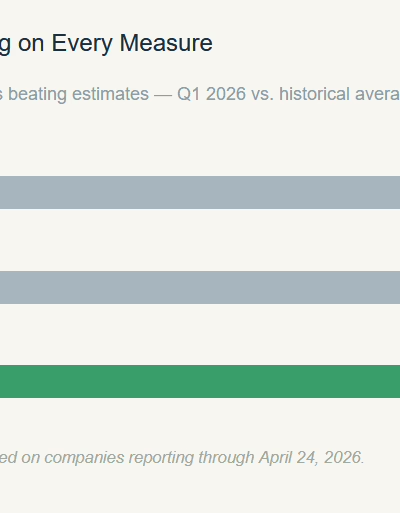

Crucially, the selloff was geopolitically driven — not a reflection of deteriorating fundamentals. Corporate America continues to deliver. Q1 2026 is projected to mark the sixth consecutive quarter of double-digit earnings growth, with analysts forecasting 13% year-over-year EPS expansion. Nine of eleven S&P 500 sectors are expected to report earnings growth, and revenues are projected up nearly 10%. This is a market built on a strong earnings foundation — and that foundation is getting stronger.

S&P 500 Year-over-Year EPS Growth

Consecutive quarters of double-digit earnings expansion

Q2 ’25

+10.2%

Q3 ’25

+11.5%

Q4 ’25

+13.7%

Q1 ’26 (E)

+13.0% (Est.)

Source: FactSet, Nasdaq. (E) = consensus estimate.

The Bull Market Remains Intact

S&P 500 approximate levels at key milestones since the October 2022 low

Oct ’22

3,577

Dec ’23

4,770

Dec ’24

5,881

Dec ’25

6,903

Jan ’26 ★

7,008 ATH

Now

~6,609

★ All-time high reached January 28, 2026. The bull market is up ~92% from the October 2022 low.

4 Reasons to Be Optimistic About the S&P 500 in 2026

With all that said — and I want to be clear — I remain optimistic on the S&P 500 for the rest of 2026. Here’s why.

1 AI Investment Is Accelerating

Big Tech capital expenditure on AI infrastructure is approaching $600 billion and climbing. This isn’t hype — it’s showing up in the numbers. J.P. Morgan estimates the AI supercycle will drive above-trend S&P 500 earnings growth of 13–15% for at least the next two years. The largest technology companies already account for roughly a quarter of total index earnings, and they’re forecast to deliver outsized profit gains as AI investment continues to scale. This is the most powerful investment theme in a generation, and it’s still in the early innings.

2 Earnings Breadth Is Broadening

One of the most encouraging developments is that earnings growth is no longer concentrated in a handful of mega-cap names. The remaining 493 companies in the S&P 500 recently posted their best earnings growth in years, narrowing the gap with the largest stocks. Nine of eleven sectors are expected to report growth in Q1. When the base of earnings power widens like this, it supports a healthier, more resilient market — and reduces the concentration risk that made some investors nervous in 2024 and 2025.

3 Valuations Have Reset

The Q1 pullback brought the S&P 500 forward price-to-earnings ratio down to approximately 19.9x — roughly in line with the five-year average. After the stretched valuations of late 2025 and early January, this recalibration gives the market a much healthier foundation for the next move higher. Historically, buying the S&P 500 at fair-value multiples has led to above-average forward returns. The reset we just experienced is actually a gift for long-term investors.

4 Wall Street Is Calling for Significant Upside

Every major Wall Street research firm is forecasting the S&P 500 to finish 2026 significantly higher than where we sit today. Bank of America has a year-end target of 7,100, Goldman Sachs is at 7,500, Yardeni Research is at 7,700, and Deutsche Bank is at 8,000. That implies upside ranging from roughly +7% to +21% from current levels. Analysts are citing continued earnings growth, AI spending, and a resilient U.S. economy as the driving forces. When every major firm is pointing in the same direction — and at these magnitudes — it’s absolutely worth paying attention.

Wall Street Year-End 2026 S&P 500 Targets

Current level ~6,609 · Implied upside shown in parentheses

BofA

7,100 (+7%)

Goldman Sachs

7,500 (+13%)

Yardeni Research

7,700 (+17%)

Deutsche Bank

8,000 (+21%)

Stock Market Outlook: What to Expect Moving Forward

So where does that leave us? The short-term headwinds were real — geopolitical conflict, tariff noise, and a tech sector catching its breath. But this is not a time to panic. It is a time to be thoughtful and disciplined.

I am not making major changes to client portfolios right now. The foundation of this market — corporate earnings, AI investment, broadening market participation, and a resilient U.S. economy — still looks solid for the long haul. Over the past decade, the S&P 500 has delivered a total return of approximately 277% — an annualized rate above 14% — despite experiencing double-digit declines in 2018, 2020, 2022, and 2025. Each time, the market recovered and went on to set new highs. I expect this time to be no different.

As the Middle East situation continues to stabilize and we get clarity on the tariff picture, I’d expect the market to find its footing and push higher in the second half of 2026. Q1 earnings season kicks off next week and should provide a fresh catalyst. That’s been the playbook before, and there’s no reason to assume this cycle is fundamentally different.

Related Reading from The Vodicka Group:

→ S&P 500 March 2026 Update — Staying the Course

→ Schedule a Free Portfolio Review

As always, if my outlook changes, my clients and readers will be the first to know. I’ll be back with another update soon — have a great week!

Until next time,

Michael Vodicka

Founder & Lead Advisor · The Vodicka Group

Disclaimer: This report is for entertainment purposes only. Every investor should consult with an investment advisor before making investment decisions. The Vodicka Group, Inc. is not a broker/dealer. We do not receive compensation for mentioning stocks. At various times, the clients, publishers and employees of Vodicka Group, Inc., may buy or sell the securities discussed for purposes of investment or trading.