The 2018 tax season is in full swing – and even though no one enjoys paying taxes I am about to share one of the easiest and most effective strategies to score a big tax break.

I am talking about making a contribution to an IRA – an Individual Retirement Account.

Not only is this a great way to save and invest money for retirement, it’s also a great strategy to score a big break on taxes. Today I am going to reveal the two most popular IRA accounts – and help help you figure out which vehicle is best for you.

Traditional IRA

The traditional IRA offers tax savings right now. Contributions to a traditional IRA are immediately deductible from an individuals taxable income. Let me give you an example.

Tom shows $100,000 of taxable income for 2018. At an effective tax rate of 20%, Tom owes $20,000 in federal income tax. If Tom makes a $5,000 contribution to his traditional IRA, his taxable income falls to $95,000 (100K minus 5K).

Under this scenario – Tom owes $19,000 in federal income tax – reducing his tax bill by $1,000.

These traditional IRA contributions are eligible for withdrawal at the age of 59.5. The account holder then pays income taxes on any distributions in retirement.

ROTH IRA

ROTH IRA is my favorite IRA account. Here’s why. Account holder do not get to subtract contributions from taxable income – however – distributions from a ROTH IRA in retirement are 100% tax free.

This structure offers enormous benefits to investors – particularly young ones.

For young investors, every $1 dollar invested could easily grow into $5 or $10, 20 or 30 years down the line. In this scenario, the ROTH IRA offers huge tax benefits.

With these two accounts in mind – I am going to share five fool proof pointers to help you optimize your IRA contributions for 2018.

5 Essential Details to Max Your IRA Tax Break

IRA Contributions Deadlines: IRA contributions cane be made up until your taxes are filed, which is April 15, 2019.

Tax Extensions Extend IRA Contribution Deadlines: If you file an extension to file your taxes by October 15, you also receive an extension to make a contribution to your IRA.

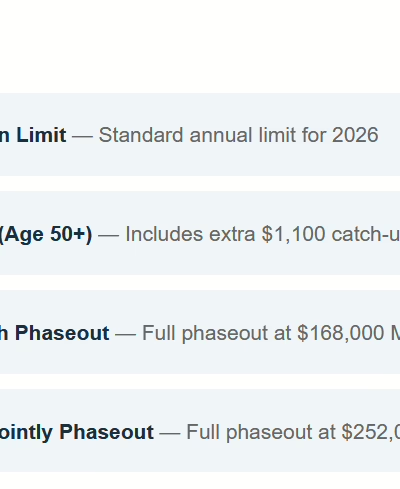

Contribution Limits: Contributions limits for 2018 are $5,500 for individuals under the age of 50 and $6,500 for individuals over the age of 50.

Income Limits for IRA Contributions: Individual tax filers making $120,000 or less can make a full IRA contribution. Joint filers making $189,000 or less are eligible for a full IRA contribution.

Joint Filers and IRA Contributions: For joint filers making $189,000 or less, each filer can make a full contribution to an IRA.

Here’s a full chart of IRA income and contribution limits from Fidelity.

How Do I Invest After Making an IRA Contribution?

After you make a smart contribution to your IRA – then you have to figure out how to invest.

In today’s global economy – it’s harder than ever to figure out where to invest. You have US stocks, international stocks, large caps, mid caps, small caps, US bonds, foreign bonds, IPOs, currencies and commodities. Its’ overwhelming for most people.

The reality is that most investors don’t have the time or experience to invest well.

If you need help investing your IRA contributions – send me an email – I can help.

You will have an expert on your team with almost 20 years of experience in the financial services industry.

- mike@vodickagroup.com

- mikevodicka@gmail.com

Your Investment Partner,

Mike

This report is for entertainment purposes only. Every investor should consult with an investment advisor before making investment decisions. The Vodicka Group, Inc. is not a broker/dealer. We do not receive compensation for mentioning stocks. At various times, the clients, publishers and employees of Vodicka Group, Inc., may buy or sell the securities discussed for purposes of investment or trading.