April 2026 · Michael Vodicka · 4 min read

The Backdoor Roth IRA is a completely legal, IRS-approved tax strategy that allows high-income earners to get money into a tax-free Roth account — even when the front door is locked. Here’s how it works in 2026, the pros and cons, and who should consider it.

What Is a Backdoor Roth IRA?

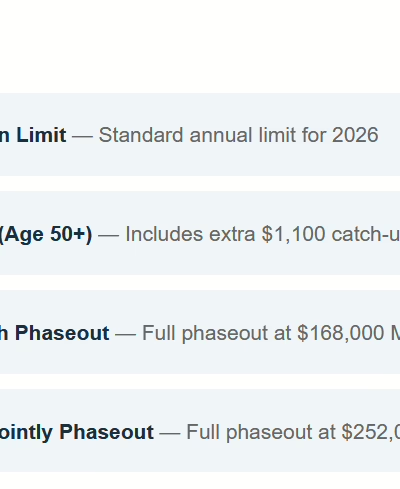

A Roth IRA is one of the best retirement accounts out there — your money grows tax-free and you pay zero federal income tax on qualified withdrawals. The problem? The IRS locks the front door if you earn too much. In 2026, if your income exceeds $168,000 (single) or $252,000 (married filing jointly), you can’t contribute directly.

The backdoor Roth IRA is a simple two-step workaround: you contribute to a traditional IRA (no income limit), then immediately convert those funds to a Roth IRA (also no income limit on conversions). You go through the back door to end up in the same place.

How the Backdoor Roth IRA Works — 3 Simple Steps

Up to $7,500 in 2026 ($8,600 if 50+). You won’t take a tax deduction — this is a non-deductible contribution.

Transfer the funds to your Roth, ideally within a few days. Since you already paid tax on the money, the conversion is generally tax-free.

Your money grows tax-free in the Roth, and qualified withdrawals in retirement are completely tax-free. No required minimum distributions during your lifetime.

2026 Key Numbers

The Pros

The Cons

Who Is the Backdoor Roth IRA Best For?

The backdoor Roth IRA is not for everyone. It works best when a specific set of conditions line up:

★ Ideal Candidate Checklist

● Your income exceeds the Roth IRA limits ($168K single / $252K married)

● You have no existing pre-tax balances in traditional, SEP, or SIMPLE IRAs

● You’ve already maxed out your 401(k) and want additional tax-advantaged savings

● You expect your tax rate in retirement to stay the same or go higher

● You want tax diversification — a mix of pre-tax and tax-free income in retirement

“If you have pre-tax money sitting in a traditional IRA, don’t attempt a backdoor Roth without talking to an advisor first. The pro-rata rule can turn a tax-free strategy into a taxable headache.”

— Michael Vodicka, The Vodicka Group

Bottom Line

The backdoor Roth IRA can be a genuinely valuable tax strategy — for the right people. If you’re a high-income earner who has been locked out of direct Roth contributions, and you don’t have existing pre-tax IRA balances complicating the picture, this is one of the most efficient ways to get money into a tax-free account. It won’t make or break your retirement on its own — the annual contribution limits are modest — but done consistently over many years, the tax-free compounding can add up to something meaningful.

As with any tax strategy, execution matters. The pro-rata rule, the paperwork, and the timing all need to be handled correctly. If you’re thinking about whether a backdoor Roth makes sense for your situation, I’d encourage you to talk it through with a qualified advisor or tax professional before making any moves.

Related Reading from The Vodicka Group:

→ S&P 500 Q1 2026 Update: Through the Storm, Into Clear Skies

→ S&P 500 March 2026 Update: Staying the Course

→ Schedule a Free Portfolio Review

Thanks for reading — have a great week!

Until next time,

Michael Vodicka

Founder & Lead Advisor · The Vodicka Group

Disclaimer: This report is for educational purposes only and does not constitute tax, legal, or investment advice. Every investor should consult with a qualified tax professional or financial advisor before implementing any tax strategy. The Vodicka Group, Inc. is a Registered Investment Advisor. Tax laws are subject to change.