May 2026 · Michael Vodicka · 5 min read

There’s a brand new senior bonus deduction worth up to $12,000 sitting on the table for older Americans — and most retirees have never heard of it. Created by the One Big Beautiful Bill Act and available for tax years 2025 through 2028, it’s one of the most meaningful retiree tax breaks passed in years. Here’s exactly who qualifies, the income phase-outs to watch, and the hidden 6% surtax trap that could quietly cost you thousands.

What Is the Senior Bonus Deduction?

The senior bonus deduction is a new federal tax break created by the One Big Beautiful Bill Act (OBBBA), which was signed into law on July 4, 2025. It gives Americans age 65 and older an extra $6,000 deduction on their federal income taxes — and married couples where both spouses are 65 or older get $12,000.

What makes it different from other senior tax breaks is that it stacks on top of everything else. You can claim it whether you itemize or take the standard deduction. It’s in addition to the regular standard deduction. And it’s in addition to the existing senior add-on that older filers already get.

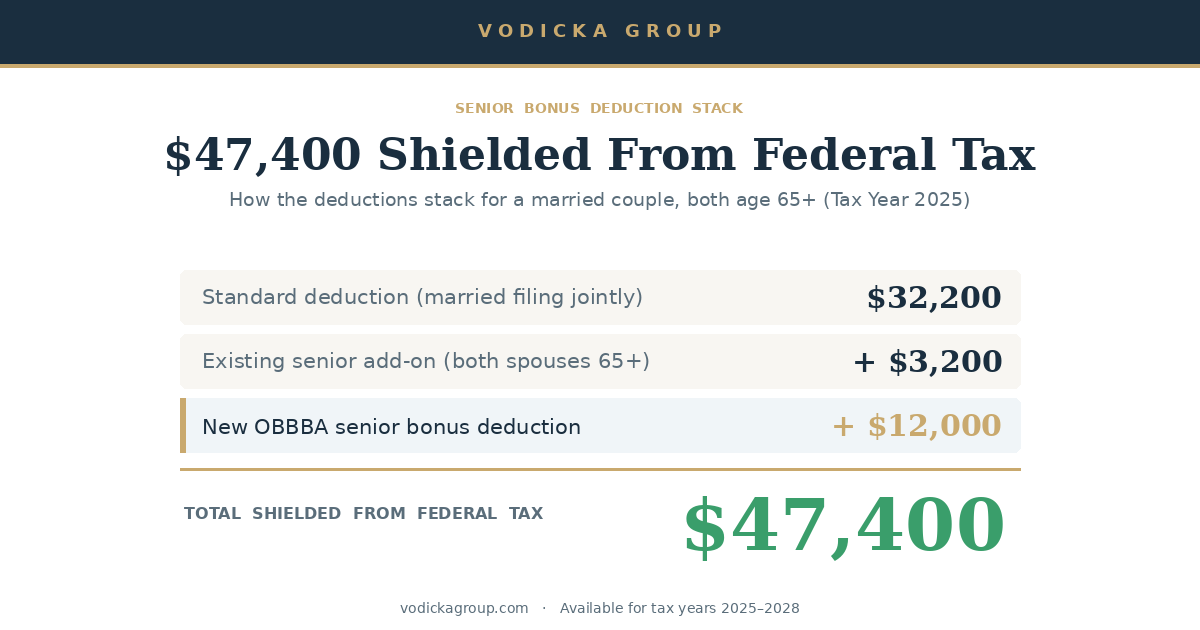

The Total Deduction Stack for Retirees

For a married couple where both spouses are 65 or older, the math adds up fast. Here’s how the deductions stack for the 2025 tax year:

$32,200

+ $3,200

+ $12,000

$47,400

2025-2028 Senior Bonus Deduction: Key Numbers

Who Qualifies for the Senior Bonus Deduction?

There are four basic rules that determine eligibility. All of them have to line up:

The Hidden 6% Surtax Most People Miss

Here’s the part most retirees aren’t told about. The phase-out doesn’t just reduce your senior bonus deduction — it creates an effective surtax on every dollar of additional income inside the phase-out zone.

What the Senior Bonus Deduction Actually Saves You

The dollar value of any deduction depends on your tax bracket. Here’s what the full $6,000 senior deduction is worth at common retiree income levels:

Single Filer (65+, full $6,000 deduction)

$720 / year

$1,320 / year

Married Couple, Both 65+ (full $12,000 deduction)

$1,440 / year

$2,640 / year

Over the full four-year window (2025 through 2028), that adds up to $10,000 or more in cumulative tax savings for a typical retired couple in the 22% bracket. For households near the phase-out thresholds, the difference between getting the full benefit and losing it entirely often comes down to careful income planning.

“This is one of the most meaningful tax breaks for retirees passed in years — but it’s also one of the easiest to underclaim. A single income misstep in the phase-out zone can leave thousands of dollars on the table.”

— Michael Vodicka, Vodicka Group

Three Senior Bonus Deduction Planning Moves to Consider

If you’re 65 or older — or you have a spouse who is — here’s where to focus your senior bonus deduction planning:

★ The Senior Bonus Action Checklist

Bottom Line

The senior bonus deduction is a meaningful piece of tax relief for older Americans — and the kind of provision that quietly puts thousands of dollars back into the pockets of people who qualify. For a married couple both 65 or older in the right income range, it can mean $10,000 or more in cumulative tax savings over the four-year window.

But the rules are nuanced. The phase-out math, the hidden 6% surtax, the interaction with Roth conversions and RMDs — these are the kinds of details that quietly determine whether a retiree captures the full benefit or leaves thousands on the table. If you’re 65 or close to it, this is a year to make sure you have a clear picture of where your income sits relative to the phase-out thresholds — and to plan your withdrawals, conversions, and capital gain realizations with that picture in mind.

As with any tax strategy, execution matters. If you’d like to talk through whether you’re capturing the full $6,000 senior bonus deduction — or whether there’s planning work to do before year-end — I’d encourage you to schedule a free portfolio review.

Related Reading from Vodicka Group:

→ Backdoor Roth IRA Explained: How It Works, Pros & Cons, and Who It’s Best For in 2026

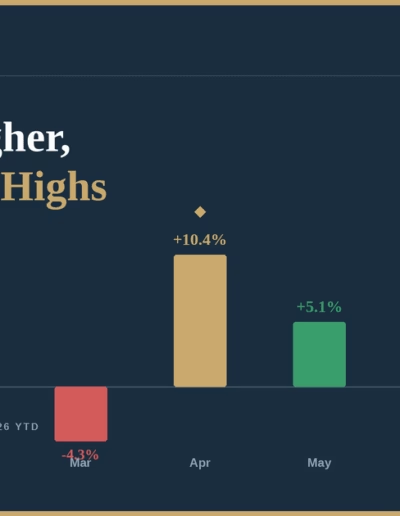

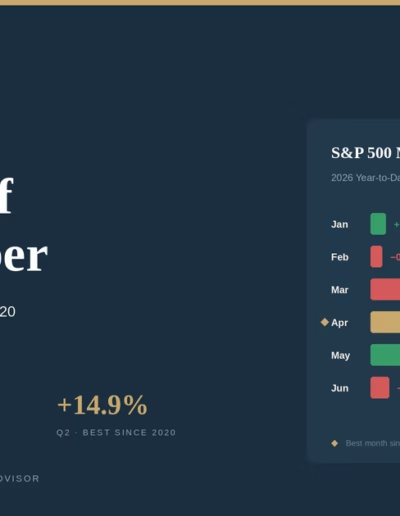

→ S&P 500 April 2026 Update: A Blockbuster Month for Stocks

→ Schedule a Free Portfolio Review

Thanks for reading — have a great week!

Until next time,

Michael Vodicka

Founder & Lead Advisor · Vodicka Group

Disclaimer: This report is for educational purposes only and does not constitute tax, legal, or investment advice. Every investor should consult with a qualified tax professional or financial advisor before implementing any tax strategy. The Vodicka Group, Inc. is a Registered Investment Advisor. Tax laws are subject to change.