The huge spike in interest rates in the last 12 months just claimed its latest victim.

On Friday, Silicon Valley Bank (NASDAQ: SVIB), the 16th largest bank in the country and a top lender to Silicon Valley, was shut down by federal regulators after a big wave of withdrawals left the firm insolvent. Here are some more details from CNBC.

“On Wednesday, Silicon Valley Bank was a well-capitalized institution seeking to raise some capital. Within 48 hours, a panic induced by the very venture capital community that SVB had served and nurtured ended the bank’s 40-year-run.

Regulators shuttered SVB Friday and seized its deposits in the largest U.S. banking failure since the 2008 financial crisis and the second-largest ever. The company’s downward spiral began late Wednesday, when it surprised investors with news that it needed to raise $2.25 billion to shore up its balance sheet.

What followed was the rapid collapse of a highly-respected bank that had grown alongside its technology clients. The episode is the latest fallout from the Federal Reserve’s actions to stem inflation with its most aggressive rate hiking campaign in four decades.”

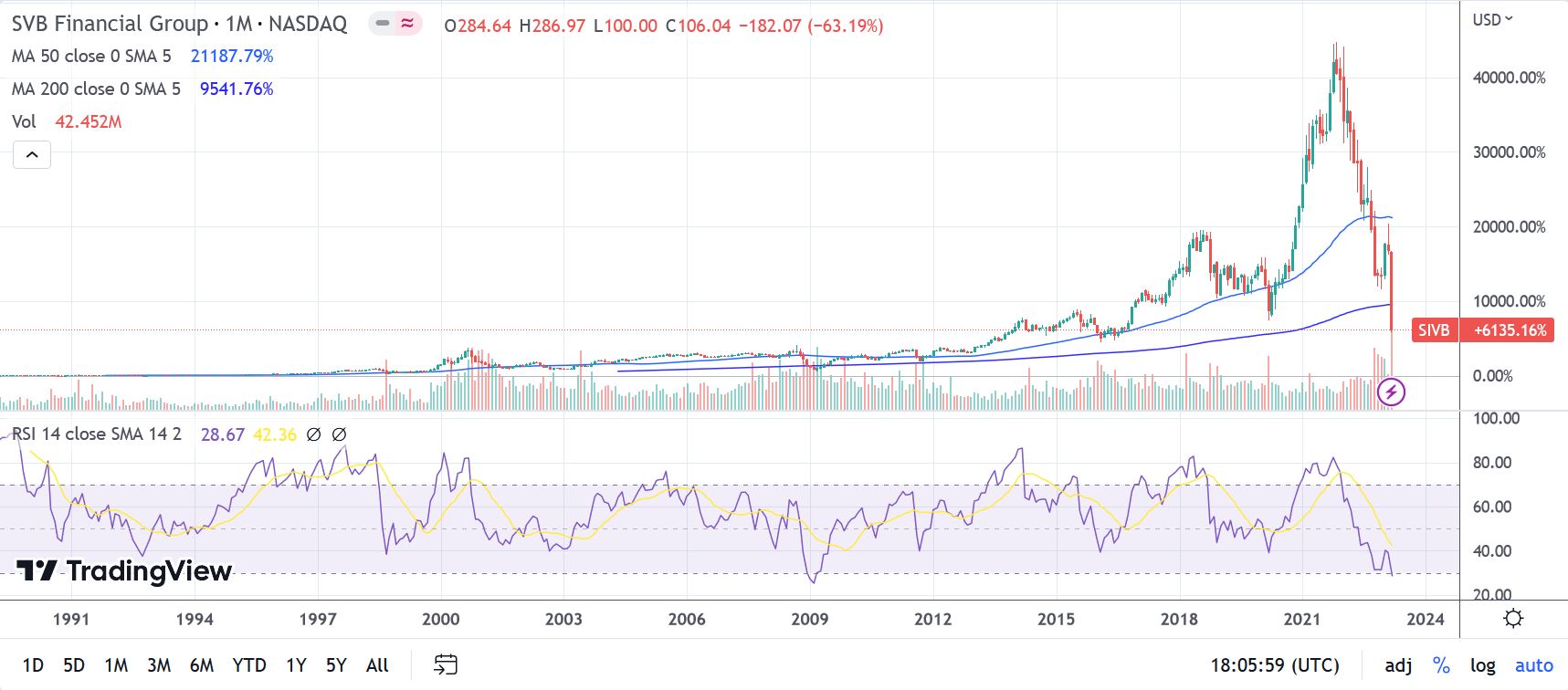

Take a look at the stunning collapse in share price in the chart below.

*chart from tradingview.com

*chart from tradingview.com

For the time being it looks like the damage is mostly contained. I am not expecting the failure of SVB to trigger another financial crisis. However investors are understandably nervous about more fallout in the banking sector.

That’s why I am dropping in today – I am going to outline how brokerage firms are specifically designed to protect their client accounts and funds in the event of a bankruptcy.

4 Safeguards Brokers Must Follow to Protect Investors

- At the highest level, brokerage firm failure is extremely rare. It is much less common than bank failure. That’s because brokers are regulated very differently than banks. Banks use fractional banking where clients funds are co mingled into a general fund, and that cash is then used for investing or lending to generate revenue for the bank. Brokers are required to keep all client funds in segregated accounts and there is no lending or investing of these funds.

- In the highly unlikely event of broker failure, client assets such as stocks and bonds are protected. These customer assets would be transferred to an outside brokerage firm where customer would regain access to securities. Remember, when you own a stock or bond you basically get a digital certificate. Brokerage firm is providing custody services for that certificate for their customers. So even if brokers fails, customers are not losing ownership or access to their stocks and bonds.

- If securities go missing from the account, federal protection kicks in, in the form of SIPC (Securities Investor Protection Corp) Insurance. This federal insurance pays up to 500K for misplaced securities.

- If client has cash in brokerage account that is misappropriated in a brokerage failure or any situation in general, the SIPC offers $250,000 in protection.

This is a high level view on how brokerage accounts are regulated and structured. These protocols have been established to protect brokerage firms and brokerage accounts from unexpected shock waves in the economy.

Looking forward, even if we do see more volatility in the banking sector, the brokerage industry should be in good shape to weather the storm. And brokerage accounts in specific are structured in a way that protects the account holder from these shock waves or even a bankruptcy.

If you would like to learn more about how brokerage accounts are protected, here are a few articles.

If a Brokerage Firm Closes its Door

What Happens if Your Broker Goes Bankrupt?

I’ll be back with another update next week – have a great day!

Disclaimer: This is not investment advice. This report is for entertainment purposes only. Every investor should consult with an investment advisor before making investment decisions. The Vodicka Group, Inc. is not a broker/dealer. We do not receive compensation for mentioning stocks. At various times, the clients, publishers and employees of Vodicka Group, Inc., may buy or sell the securities discussed for purposes of investment or trading.